Back

Pay Your Way

The future of payments is digital. From bitcoins to digital wallets, social shopping, and more. Here are the top 10 payments trends to consider in the years to come.

Back

Pay Your Way

The future of payments is digital. From bitcoins to digital wallets, social shopping, and more. Here are the top 10 payments trends to consider in the years to come.

The first time I saw someone use their smartwatch to pay for their groceries, I knew everything had changed. I really had to think just how much of our lives are now digital – how we communicate, watch movies, listen to music, work, and now, even how we pay for things.

- Foreword

- Introduction

- Trend 1: Buy Now, Pay Later

- Trend 2: Open banking

- Trend 3: Biometric authentication

- Trend 4: Cryptocurrency

- Trend 5: Super apps

- Trend 6: Social shopping

- Trend 7: Green payments

- Trend 8: The metaverse and digital assets

- Trend 9: Unified and connected commerce

- Trend 10: Digital payments

- Positive disruption

- Sources

Foreword

Of course, cash isn’t going to disappear overnight. I can’t imagine a world where I won’t be stuck behind someone slowly counting out coins at the cash register! But it’s clear that the convenience of digital payments is seeing businesses of all shapes and sizes introduce their own solutions.

During the next years it’s inevitable that we’ll see a bigger transition away from cash as more people go from ‘sometimes’ using cash to rarely needing it. Younger generations will drive this change. Every business will need to accept that reality.

How we pay is evolving.

But this is the nature of modern payments. We’ve moved from cash registers to Point of Sale systems (many of which are now cloud-based and even built within smartphones1), gone from using a PIN to tapping our cards to pay. We can easily transfer money from our accounts using an app. If we don’t want to pay bank charges every time we pay, we can link our account to an Apple Pay, Google Pay, or PayPal account.

I’ve even read how companies are developing microchip implants to insert under the skin2. You can then make contactless payments without needing a card. Not that I’ll be doing that any time soon!

For me, this is a clear indication that it won’t be long before even our trusted cards will be a memory. Linking our accounts to an app means we can pay with any device, whether a phone, a tablet, or even a watch.

“That’s pretty amazing.

Today we’re experiencing a digital revolution when it comes to payments. Just imagine what tomorrow will bring.”

Georg Hansbauer, CEO & Co-Founder, Testbirds

Introduction

The world of payments is rapidly changing.

In their World Payments Report 2021, Capgemini3 noted how the financial industry is now transforming into Payments 4.X – “an experience-driven environment that’s witnessing even more industry consolidation and attracting tech-expert ecosystem players.”

This is an environment where payments, which were once mainly focused on being quick, easy, and invisible, must now also be frictionless, seamless, and provide an immersive customer experience. It’s a new era being driven by changing consumer behavior and expectations, but it’s next-generation technology, combined with digital disruption, which is powering the move.

Additionally, it’s enabling B2C and B2B segments to utilize more flexible payments solutions as traditionally underserved small-to-medium-sized businesses can now make better use of these agile technologies.

As business transforms into this so-called Payments 4.X era, in the end, it all comes down to providing convenience and letting consumers take more control of how they pay and receive payments. To give them more personalized choices. Social shopping, for example, is set to let people purchase items from where they spend considerable time online, and where they can immediately ask for recommendations and comments directly from their friends and family. For those who want to know more about the environmental impact of their purchases, green payments will enable users to donate to eco-friendly partners.

These technologies are also enabling newer entrants to develop financial products and services that are challenging established financial institutions. Some may develop solutions that enable businesses to minimize or remove the cost of ‘swipe fees’ for online transactions4, others may incorporate convenient QR-code payments or offer digital invoicing.

And yet, conversely, they are also enabling banks to develop innovative options, such as ‘stablecoins’, which may provide them with yet another competitive advantage.

“If you think nobody cares about you, try missing a couple of payments.”

STEVEN WRIGHT

This new world of payments will have its challenges, particularly with cybersecurity and regulations, but as our world becomes more connected through digital solutions, one thing is certain, it is a clear signal that the cash-less society is steadily becoming a reality.

With this in mind, let’s look at 10 of the biggest payments trends to look out for in the coming years.

Trend 1: Buy Now, Pay Later

For consumers looking to make a purchase but who do not want (or can’t) pay for it in one go – or who don’t want to use a credit card owing to interest fees – installment-based payments are an increasingly popular option. Such Buy Now Pay Later (BNPL) solutions offer unsecured credit and allow customers to buy online or in-store without having to pay the complete amount upfront. Requiring less detailed retail credit checks than other forms of retail credit, BNPL is booming. According to Grand View Research, BNPL was “valued at USD 4.07 billion in 2020 and is expected to expand at a compound annual growth rate (CAGR) of 22.4% from 2021 to 2028”.5

Such growth is easy to understand. By offering consumers (even those with limited or low credit) a simplified payment option, fixed payments, and no interest fees, they can avoid lending options that are too expensive or restrictive. It also entices consumers to spend more than they normally would. This was expanded on in the Grand Review Research’s BNPL Market Analysis Report:

“These solutions also allow customers to spend more than they can with other payment methods. According to a survey of 6,500 adults conducted by Cardify in 2020, around 44% of customers said that BNPL solutions play an important role in determining how much they spend over the holidays. Moreover, around 48% of customers said that BNPL solutions allow them to spend 10% to 20% more than they would by their credit card.”

For BNPL providers, this requires being able to assess credit risk, balance the cost of funds, deal with regulations, and manage bad debts. And for traditional solutions, unless they develop their own solutions, they will need to partner and/or purchase solutions that will enable them to compete for the same business.

This will happen as consumers view banks as a trusted lending resource. For others, building trust is essential. Especially as retail giants, such as Amazon, already offer BNPL. This will require that merchants will need to do their due diligence in finding a trusted, transparent, and convenient funding service – alongside a solution that they can easily and cost-effectively install alongside their existing checkout process.

But as more people purchase online, it’s certain that BNPL will soon be everywhere.

Trend 2: Open banking

It is impossible to discuss digital transformation without talking about open banking. By making use of Account Information Services (AIS), open banking enables consumers to securely share sensitive information with trusted third parties. This is pushing the development of truly innovative financial solutions – while being a catalyst to the growth of fintechs and their development of products that can effectively work with banking services.

In addition to AIS, Payment Initiation Services (PIS) are offering acquirers a variety of opportunities by enabling service providers to create new and innovative payment solutions. Their potential is only now being fully explored, which comes as no surprise with improved technology, robust 5G networks, the Payment Services Directive in the EU opening the financial market to third-party providers, and consumers purchasing more online.

Payment Initiation Services have clear benefits for both merchants and consumers, as noted by London-based, Modulr Finance6:

“PIS benefits for merchants:

- Transactions settle instantly rather than the three day average for card transactions, a significant cash flow improvement

- PIS can prove to be more secure than card payments, reducing funds lost to fraud

- PIS can be an opportunity to lower acquiring costs – based on our market research, PIS’s can be more cost effective for transactions above £50

PIS benefits for consumers:

- They don’t have to remember and input a card number

- Have increased security of their payment details (as merchants do not store any payment credentials)

- The experience will become smoother and more intuitive, with increasing support of app-to-app authentication.”

Ultimately, it will be PIS that challenges payment cards. Time will tell whether they can fully replace them, but it is certain they will become a strong complement to them. As more people shop online and as more merchants offer immediate settlement and an improved customer experience, it is an area worth keeping your eye on.

Trend 3: Biometric authentication

Beyond the expectation of security, consumers expect payment solutions that are interconnected and easy to use. For merchants, this is spurring an intensive search for solutions that provide such a seamless experience, help avoid cart abandonment, and provide simplified and safe transactions – whether in-store or online.

Biometric authentication and behavioral pattern recognition are leading the way. Whether using a fingerprint, their face, eye (iris), vein patterns, or even their voice, payments can be made without the need for PIN authentication. Most commonly, this is found on mobile devices but is increasingly being seen with payment authentication. And in today’s pandemic-conscious world, contactless convenience has clear benefits.

Traditionally, authentication has revolved around something a user knows, such as a password or PIN. As digitally-powered smartphones and their associated apps have become more widespread, this has evolved into the phone itself being their authentication. With biometrics, this is further evolving into ‘something that is the user’ being the sole authenticator (such as a fingerprint).

This includes biometric data that goes beyond physical identifiers and moves into a person’s other unique characteristics, such as how the keystrokes are made on their phone’s keyboard. Through a combination of machine learning, big data, and risk assessment techniques, unique patterns can be identified to distinguish between a real user and a potential fraudster.

As consumers grow tired of the endless number of authentication methods, they need1 while making a purchase or banking (ever more complex user/name passwords, two-factor authentication, etc.), behavioral and biometric methods are sure to gain in popularity. Especially as their behaviors and movements can be learned in more detail over time, which will reduce the number of transactions that may be blocked.

This can ensure, whether through shopping or banking, that the consumer enjoys a seamless, personalized experience without multiple verification steps.

Solution

Customer Journey Testing

The line between the real and digital world continues to fade. Test interactions in all parts of the customer experience with the help of the Crowd, and in real-world conditions.

Find out more

Trend 4: Cryptocurrency

Exploding into the popular consciousness these past few years, cryptocurrency is steadily gaining traction within mainstream financial services. While most people have heard of Bitcoin (still very much the top-valued cryptocurrency), other versions include Ethereum, Binance Coin, and Cardano. Based on blockchain technology, crypto was initially envisioned to be a form of a decentralized currency that sidesteps government oversight and traditional banking fees.

Today, however, cryptocurrencies are more aligned to speculative investments that are publicly traded – and their value is decided by supply and demand. Currently, its overall volatility, and the challenges in converting it into other forms of payment, have seen little merchant interest in cryptocurrency.

For example, organizations such as Paypal2 and Visa3 allow users to hold, sell, and buy several cryptocurrencies, but they are not used as payment options.

This is likely to change as agile fintechs, central banks, and other financial institutions invest in the development of a more stable form of cryptocurrency. As noted in the 2021 McKinsey Global Payments Report4:

More“The European Central Bank announced recently it was progressing its ‘digital euro’ project into a more detailed investigation phase. More than four-fifths of the world’s central banks are similarly engaged in pilots or other central bank digital currency (CBDC) activities. Concurrently, multiple private, stabilized cryptocurrencies—commonly known as stablecoins— have emerged outside of state sponsored channels, as part of efforts designed to enhance liquidity and simplify settlement across the growing crypto ecosystem.”

Each stablecoin is linked to a particular asset, such as the country of origin’s currency. They are, unlike Bitcoin, issued by private and/or public institutions and are not able to be redeemed and mined with permission. But being linked to a centralized asset means the value of the stablecoin is far more stable. One of the first to develop such a stablecoin, is JPMorgan Chase, with their JPM Coin5.

This is not to say each effort is a guaranteed success. A significant issue with stablecoins are the regulations that follow them. Most recently, Facebook’s Diem coin6, citing an inability to progress with regulators, ended operations and was sold to a bank holding company.

It is a special form of stablecoin, the Central Bank Digital Currency, which is likely to become the future of digital currency and payments. Issued and controlled by a country’s central bank, a CBDC is a digital form of that country’s fiat currency. It is this stability that makes them ideal for payments – and the safer bet for anyone developing purchasing solutions for cryptocurrency.

Show lessTrend 5: Super apps

The old saying ‘one for all and all for one’ is particularly relevant when it comes to super apps. Already popular in Asia, these all-in-one apps are set to become a predominant feature on digital devices around the world.

The concept behind super apps is simple. Rather than someone having to use a range of individual apps to do one specific thing, a super app combines everything into one. Have food delivered, communicate with friends, order a taxi, pay for goods, connect with your bank, and far more.

Super apps can be immensely broad in their scope (in the hope of providing everything, such as Uber’s recent efforts7), whereas others focus on specific segments like financial services. For example, in 2021, PayPal announced its plans to morph its Venmo (a peer-to-peer digital payment brand) and other mobile apps to create a ‘one-stop shop’ for consumers’ financial needs (including offering merchants QR-code functionality and Buy Now Pay Later options)8.

This multifunctionality has clear benefits. Users don’t need to find a specific app for a certain function or have multiple accounts (with numerous usernames and passwords), and their overall experience can be more convenient, simplified, and seamless.

A super app developer, on the other hand, can utilize a ‘mini program’ (sub-application) to run on their interface that does not need to be downloaded. WeChat, for example, which started as a simple chat tool has transformed itself into a true super app with over 1 billion users and offering more than 1 million mini-programs.9

For such a business, all payments can come through one centralized system and there is no need for extensive marketing. A simple push notification can reach all users, regardless of the apps they use. Extensive data can also be collected to gain a more holistic view of their needs, offer better-customized solutions, and fully understand what works – and what doesn’t – throughout their customer journey across multiple services – whether it’s buying clothes or transferring money.

In our ever-connected world, this is one area that will see huge gains in the coming years.

Trend 6: Social shopping

To say that social shopping (or social commerce) is trending would be an understatement, as was noted by Accenture:

“In just one day in October 2021, two of China’s top live-streamers, Li Jiaqi and Viya, sold $3 billion worth of goods. That’s roughly three times Amazon’s average daily sales. This is the power of social commerce. And it’s set to sweep the world, growing into a $1.2 trillion wave of change by 2025.”10

While these numbers were certainly driven by the coronavirus pandemic’s lockdowns – and people’s need to find alternative means of socializing and shopping when they couldn’t go outside – social shopping shows no sign of slowing down. As the old saying goes, you can’t put the genie back into the bottle.

Especially with many of the world’s largest platforms becoming involved, including Facebook, TikTok, Instagram, Pinterest, and even YouTube and Twitter.11 For anyone involved in e-commerce, partnering up with any of these platforms and gaining access to their millions of followers, can bring substantial benefits.

It would, however, be too simplistic to consider social shopping as an extension of any number of social media platforms. It is also about how any brand – whether online or bricks-and-mortar – can use the power of social connections to build its brand.

Consider the Burberry ‘social experience’ in their Shenzhen, China store. Combining a traditional brick-and-mortar experience with technology, “The concept, which is the first step in an exclusive partnership with Tencent, takes interactions from social media and brings them into a physical retail environment. Through a dedicated WeChat mini-program, customers can unlock exclusive content and personalized experiences and share them with their communities.”12

In today’s reality, such a blend of in-person and social media can be utilized by any organization, from something as big as a sports team’s merchandising that can be promoted on the smartphones of everyone in the stadium, to a restaurant offering a contactless menu that can be shared online, or to any brand offering an ambassador program.

As online social connections gain in popularity and as more consumers shop online, building a payments solution that considers social media is something everyone will ‘like’.

Trend 7: Green payments

Even as consumers increasingly pressure businesses to be more environmentally friendly and sustainable, a range of initiatives and regulations are being introduced around the world to encourage businesses to create a positive impact. These include Environmental, Social, and Governance initiatives13 and the United Nations’ 17 Sustainable Development Goals14, which are meant to be addressed by 2030.

Most recently, after the Intergovernmental Panel on Climate Change declared in early 2021 that climate change was now “code red for humanity”15, the 26th UN Climate Change Conference of the Parties (COP26) was held in Glasgow16 later that year. This meeting helped to solidify governmental action on the climate emergency, which will certainly involve businesses of all sizes.

With everyone being increasingly serious about climate change, this is seeing a range of payment innovations appear. For example, the new Visa Eco Benefits, “a new package of sustainability-focused benefits for account issuers designed to enable and encourage their cardholders to engage in sustainable consumption behaviors.”17

The program includes:

- A carbon footprint calculator

- Carbon offsets

- Personalized education for customers

- Sustainable card materials and digital receipts

- Donations to environmental organizations when Visa cards are used

- Expanded rewards for cardholders for sustainable behaviors

Additionally, there’s IDEMIA, a global leader in identity technologies, who have introduced their GREENPAY18 sustainablepayment solutions, which” encompasses products, services, processes and carbon emission offsetting programs to help financial institutions achieve their sustainable development goals.”

While good for business and a strategic way to boost customer engagement, shareholder approval, and to even motivate employees, offering solutions that let everyone track and manage their environmental goals, is good for the planet.

Trend 8: The metaverse and digital assets

There’s no doubt that the metaverse has been one of the biggest business buzzwords of the past year. Aiming to blend virtual and augmented reality into a shared environment (that is, a new sales platform), the metaverse is an ambitious concept that lets people socialize, shop, and interact with others and digital 3D objects.

Currently, one substantial obstacle for true immersion is affordable access to virtual reality accessories, such as Oculus Quest 2 headgear. Not that it is required for all things metaverse.

But huge investments from organizations, such as Meta (Facebook) are pushing this brave new digital world into reality. Facebook’s metaverse game, Horizon World (“a social experience where you can explore, play and create.”19), and their online meeting/collaboration Horizon Workrooms20, are leading the way.

What is clear, is that two things will be required to make the metaverse function – the development of digital assets and money. Cryptocurrency, alongside non-fungible tokens, will have a role to play. However, it is the development of digital real estate that will form the backbone of the metaverse, where real-world elements are recreated in virtual form. A store21. A concert hall22. An exhibition.23

Overall, it’s worldbuilding that creates a place to display, promote, and sell goods or services. And when what can be created is limitless, so are the potential benefits to merchants.

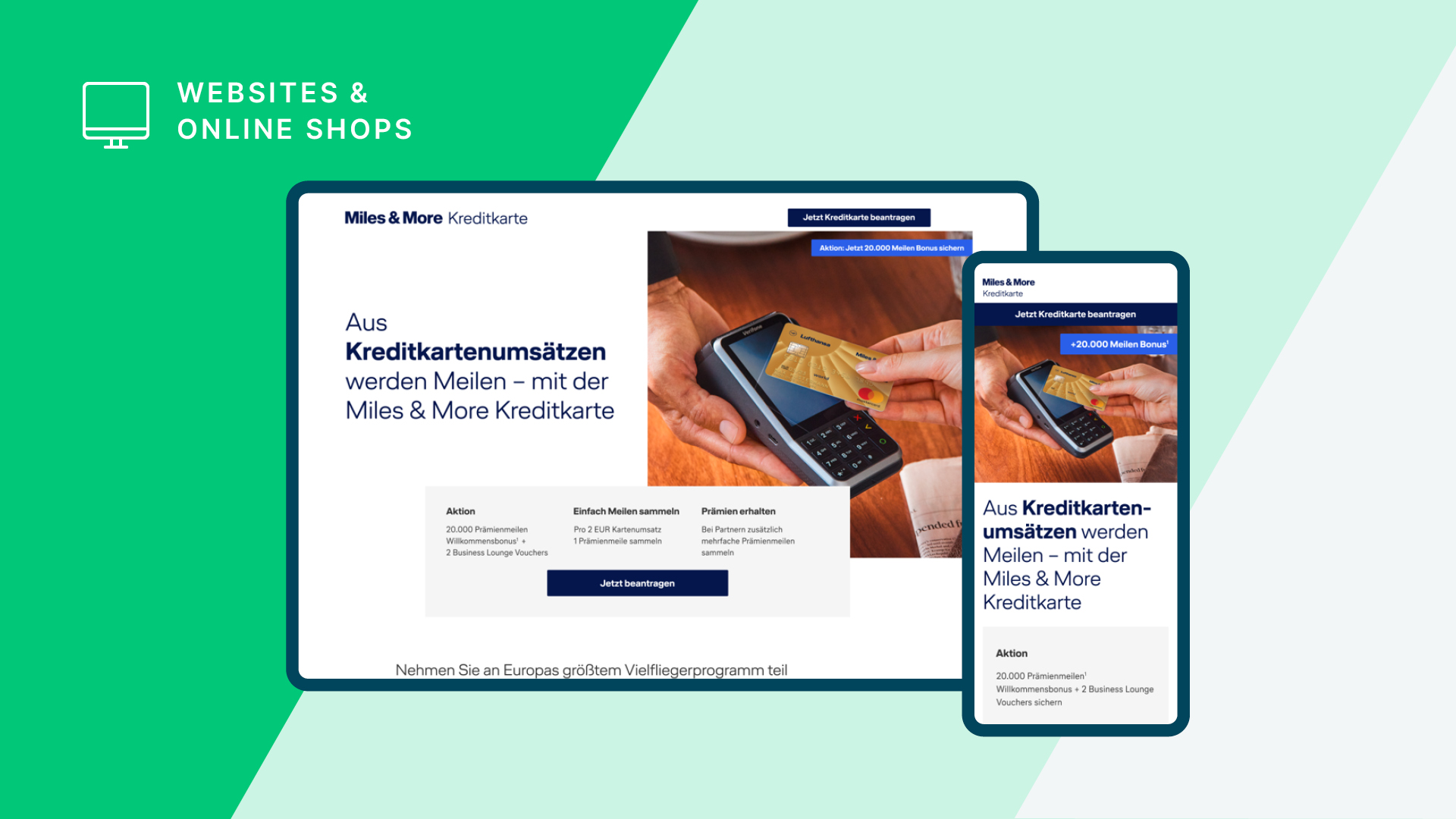

Case Study

Miles & More credit card: Usability testing of campaign landing pages

Trend 9: Unified and connected commerce

When it comes to the customer journey, it’s a trend that never ends. While omnichannel tends to get all the press, unified commerce, and connected commerce are increasingly seen as essential to the development of a truly personalized and seamless customer experience.

Of all the benefits of an omnichannel experience, one area tends to be lacking. Real-time updates to information. This is what unified commerce aims to correct. Typically, when a customer requests an item, back-end systems (or an employee) check that it is available. However, with omnichannel, there is no guarantee that the item is in stock. It may appear it is, but the front-end system may not have been updated to show it isn’t.

Unified commerce aims to provide a clear view of what is true by merging channels and not just connecting them. That the backend is fully connected to customer-facing (front-end) systems via a single platform that can better support omnichannel journeys.

Connected commerce, on the other hand, looks to complement both omnichannel and unified commerce by linking all commerce solutions (from loyalty programs, payment options, operational data, marketing, and more) across online solutions, Internet of Things devices, and anything else that may improve and enhance the customer experience. This can ensure consistency across all channels and provide a huge amount of information, which can then be used to discover actionable insights – and in many ways, help drive innovation.

Whether through a dedicated platform24 or an integration of technologies into a variety of products, the end goal is to develop solutions that meet customer needs and expectations wherever, whenever, and however they shop. Consider Amazon Go’s cashier-less checkouts25. Or Samsung Connected Spaces26 – a “a pop-up shop solution outfitted with cutting edge retail technology”.

Trend 10: Digital payments

The past two years of pandemic disruption has resulted in merchants having to develop new ways of engaging with customers. And going by the massive surge in online shopping, this has succeeded. Even as we enter a post-Covid world, many of these changes are here to stay, especially when it comes to the growing range of payment methods. Not only are they embracing digital technologies, but they are making payments more seamless and contextual.

A significant player in this field are digital wallets. An app or browser-based solution that stores multiple payment types from credit and debit cards, loyalty cards, banking information, boarding passes, anything that can be used to conduct various transactions. It is your wallet without paper money. And it’s quickly gaining in popularity. According to the 7th Worldplay Global Payments Report27, 52% of e-commerce payments took place on a mobile device in 2021. With Statista research28 showing that there are over 6.5 billion smartphone users in the world (and an estimated 7.6 billion users by 2027), digital transactions are set to increase even further; especially as people opt for more online and cash/ card-less methods of paying. Overall, the smartphone is a catalyst for this change. This was noted during a discussion on evolving business models and digital payments at the recent MWC Barcelona 202229 conference by Matija Razem, VP Business Development at Infobip, who said that the cell phone is “…at the same time an app, which you can use for payments, for banking applications, for anything. For communication. But you can also use it for identification.”

This usage is also driving another type of payment method – QR-codes. It’s easy to see why they’re increasing in popularity as QR-code payment users expected to reach 2.2 billion by 202530. They offer a simple and safe payment method that requires little more than the user scanning the code with their phone. While initially providing links to corporate websites or videos to display information about a product or service, QR-codes are now being used to provide a better customer experience.

Whether a consumer is streaming a show, watching a TV commercial, visiting an influencer’s social media page, or looking at non-digital material such as a take-away restaurant’s menu, a QR-code can be incorporated. Each can then provide additional information, enable purchase with a click, offer discounts, and more.

Positive disruption

As consumers demand more and technology rapidly evolves, disruption to merchants and the financial industry is set to continue throughout 2022 and beyond. While it is bringing numerous challenges, such positive disruption is also encouraging innovation.

This is essential as the world embraces digital money and today’s trends become tomorrow’s business as usual.

Just imagine what’s to come.

Whitepaper